Maxing ESPP Contributions on a Budget

Disclaimers: I’m not a financial advisor, and this is not financial advice, just my experience. While I developed this plan myself, it’s not an original concept and was largely inspired by discussions I saw in financial forums.

I started a new job last month and while reviewing my benefits, I remembered setting up my benefits for my first job after college and the strategies I used to maximize gains.

One of these strategies was to maximize my contributions to both my 401k and the Employee Stock Purchase Program (ESPP), which is a benefit that allows you to buy company stock at a discount. I wanted to max out my ESPP contributions and sell immediately so that I could lock in the guaranteed return of the company discount (free money!), but I didn’t have the room in my budget to afford the 10% contribution limit. So, I devised a strategy to maximize my contributions on a budget.

My strategy to remedy this and contribute the max 10% was to save up a lump sum for my contributions one time and then draw down from that savings bucket each paycheck. At the end of the purchase period my savings bucket would be zeroed out. After purchase, I’d immediately sell my shares to lock in a 15% or more discount. I’d use the sale proceeds to refill my ESPP savings bucket and put the gains towards my other financial goals! There are pros and cons to the approach I took, which I’ll outline.

ESPPs are complex, here are some definitions:

Overview:

- Employee Stock Purchase Program (ESPP): A company benefit program that allows you to buy company stock at a discount through payroll deductions.

- Offering Period: The period when payroll deductions accumulate to purchase company stock. At my company, this was 6 months, but it can range from 3-12 months.

- Employee Contribution Limit: Company limit on how much of your paycheck you can contribute to the ESPP. At my first company this was 10%, but at my current company the limit is 25%. 10%-15% is typical.

- IRS Contribution Limit: The IRS has an annual limit for ESPP stock purchases which is the total purchase price, not the price you pay based on your contributions and the discount. In 2025 the limit is $25,000, and at a 15% discount you could only contribute 85% of the limit, or $21,250. I didn’t have to worry about reaching this limit with my first job.

Purchase Details:

- Purchase Date: The date stocks are purchased with your withheld contributions at the discount rate.

- Example: If you withheld $1,000 over the period and your company had a 15% discount, you’d buy approximately $1176.47 worth of stock (15% of 1176.47 is 176.47 and 1176.47 - 176.47 = $1000).

- Discount Rate: The percentage discount offered by the company for employees in the ESPP. My discount was 15%, but 5%-15% is the common range.

- Lookback Provision: Some companies will look back to the price of the stock at the start of the offering period and use whichever price is lower, that old price or the current price to purchase the stock. This is beneficial if the stock price has gone up, since your discount becomes the discount rate + the stock price increase during the offering period. Since companies use whichever number is lower to purchase, you’re not penalized if the stock price dropped, and you’ll still get the gains from the discount rate. Here are two examples with a discount rate of 15%.

- Example: ESPP Purchase if the Stock Price Increased

- Price at Start: $10

- Price at End: $20

- Since the lookback uses the lower price of $10, you buy the stocks at a 15% discount of $10, or $8.50, which is a gain of 135% compared to the current stock price of $20.

- Example: ESPP Purchase if the Stock Price Decreased

- Price at Start: $20

- Price at End: $10

- Since the lookback uses the lower price of $10, you buy the stocks at a 15% discount of $10, or $8.50, which is a gain of 18% compared to the current stock price of $10.

- Example: ESPP Purchase if the Stock Price Increased

Taxes:

- Holding Period: The time needed to hold ESPP shares to get favorable tax treatment. The IRS-defined holding period requires you wait both 1 year from the purchase date and 2 years from the offering date (first day of the offering period).

- Disqualifying Disposition: Selling ESPP shares before meeting the IRS holding period, resulting in ordinary income tax on the discount you received at purchase (in addition to capital gains taxes if the stock price increases between your purchase and sale).

With all these definitions in mind, I’ll illustrate in more detail my strategy to maximize ESPP contributions on a budget and explain some pros and cons of my approach.

First, let’s start with an example of my strategy assuming a salary of $65,000 with biweekly paychecks and an ESPP with an employee contribution limit of 10%, with a 15% discount rate, and a 6 month offering period.

- To max out your ESPP you only need to save $3250 one time, or budget to accommodate the 10% payroll deductions for one 6 month period.

- Each purchase period, your $3250 in payroll deductions will be used to purchase stock and you’ll secure at least a 15% discount. To calculate a 15% discount where you know the final purchase price of $3250 but not the price being discounted, you can use the formula $3250/.85 = $3823. So in this example, you’d purchase $3823 of stock at a 15% discount with your $3250 of payroll contributions, netting at least $573 every 6 months, or $1146 per year. Annually, that’s an extra 1.76% of your $65,000 salary if you sell it! Keep in mind, if the plan has a lookback provision and the stock goes up, this would be more, even thousands more if the stock does extremely well.

- For my strategy with this example, after the first period where you either saved up $3250 or budgeted to accommodate the 10% deductions, you can just churn out an additional $1146+ of income per year without contributing anything new! To do this, after the first sale, where my $3250 of contributions got me $3823, I’d take the $3250 and put it in my savings account. I use Ally where you can set up savings buckets, and I had one called ESPP Contributions. The $573+ of earnings were mine to do whatever I wanted with. This amount would be taxed, so some would recommend putting aside a portion of the $573 for taxes. I used the rest to contribute to my top goals, like contributing to my Roth IRA.

- For the next 6 months, every biweekly paycheck I’d take the amount I was contributing to the ESPP from my payroll deductions out of my savings bucket to spend. In this example, with biweekly paychecks there would be 13 during the offering period, and $3250/13 works out to an even $250 that wouldn’t hit my account from payroll, but instead I’d transfer from my savings account to my checking account so I could use the money for my biweekly budget.

Overall, this plan worked really well for me. It allowed me to maximize my retirement savings in my 401k and maximize my ESPP gains. However, this strategy wouldn’t make sense for everyone, so I’ll close out by sharing some of the pros and cons.

Pros:

- Benefits of maximizing ESPP contributions

- Maximize contributions on a budget. If you can’t afford the contributions because you’re just starting your career or have a lot of priorities or expenses (paying off debt, saving for a house, kids, retirement), this is a strategy to make sure you can still get the maximum returns from your ESPP benefit.

- 15% guaranteed discount is a really good investment return in such a short period of time.

- This allows you to benefit from your company’s stock doing really well without having to gamble on buying, holding, and selling a single stock over a period of time. If your company’s stock goes way up and you have a lookback provision, you’ll get an amazing discount.

- Benefits of selling immediately

- While the stock could go up, it could also go down, erasing your 15% discount

- Selling immediately minimizes the risk of holding a single stock. As a Boglehead investor, I invest in low cost index funds so I can get market returns. I don’t have the time, energy, or expertise to try to beat the market with a single stock.

- Selling immediately and reinvesting your gains elsewhere helps you diversify (in my case, I also used the flexibility of not having to budget contributions after the first holding period to contribute more to my well-diversified 401k). You already have a big stake in the success of the company you work at, as it determines your job security and upward mobility, your bonus amount, and your ESPP discount. Holding stock from your company makes your financial portfolio less diversified, and diversification is really important. One question to ask yourself when deciding if you want to hold your company’s stock long term is if you got a cash bonus of that same amount, would you invest it in your company’s stock?

Cons:

- The main con of this strategy is that selling your ESPP shares immediately will incur more taxes than if you held for the IRS holding period for a qualifying disposition. Because of this, you’ll have to pay taxes on the discount as regular income, whereas if you wait the holding period, you pay ordinary income tax on the lesser of the discount at purchase or the gain from purchase to sale, and long-term gain taxes on any additional gains after that. Long-term gain taxes are lower than ordinary income taxes, so you minimize taxes by selling after the holding period is complete.

- For me, the combination of not being able to afford to contribute if I didn’t do this strategy combined with my hesitancy to hold my company stock for so long made it an easy decision at the time. It’s important to remember that while optimizing taxes is great, it’s almost always better to make more money even if you’ll have to pay more taxes on it.

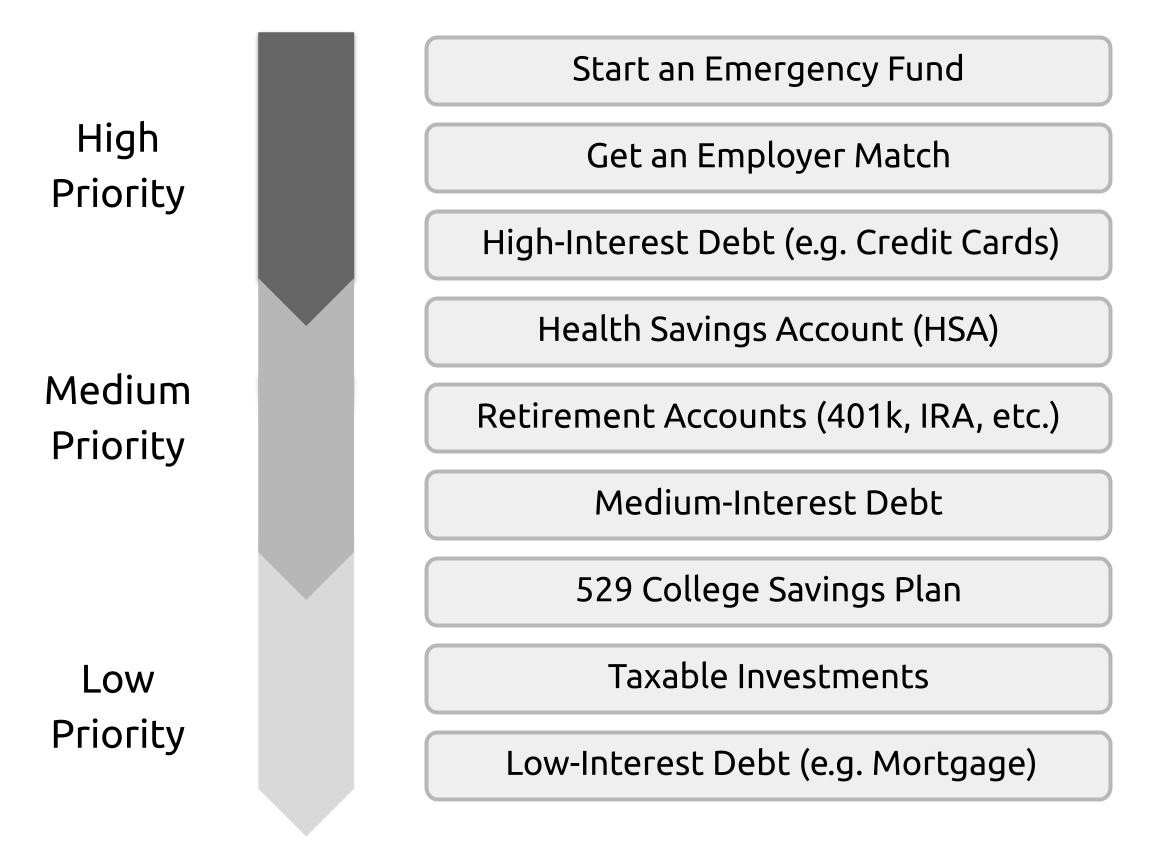

- If you have pressing financial needs like high interest debt or critical expenses, it might not make sense to save the initial lump sum or budget the contributions for a full period. I’m a huge fan of this Boglehead investment prioritization diagram, and use it myself when considering what to prioritize first. Based on this framework, the first thing you’ll want to do is start an emergency fund. You won’t have access to the ESPP contributions during the offering period, so you need to make sure you can afford any unexpected expenses. I consider the ESPP to be in line with an employer match (though you most commonly hear this in reference to the 401k match), so I think it should be a high priority, but everyone’s situation is different and crushing high-interest debt or critical expenses can take precedence.

- Another related con is that there’s an opportunity cost of locking up these contributions for 6 months. This is particularly relevant if you don’t end up purchasing at the end of the period due to withdrawing the contributions or leaving the company. The withheld money doesn’t earn interest, so if you leave the company or need to get your contributions returned to you for any other reason before the purchase, they will have gained no interest for the period, and you wouldn’t have been able to use those funds for other wealth-building opportunities like investing.

- Lastly, if your company is doing well, it’s possible you’d miss out on a lot of gains by selling the stock immediately. But as I mentioned earlier, I don’t like that gamble when I’m already so invested in the success of my company in other ways, and having a large portion of my invested assets in a single stock doesn’t align with my Boglehead investing philosophies.

So there you have it! That was my strategy for maximizing my ESPP contributions on a budget. With my benefits selection this time around I thought through the taxation element a lot more critically, because now I could afford the deductions if I wanted to. But honestly, I’m still averse to holding a large amount of my company’s stock, so I’ll probably keep selling immediately.

As you can probably tell, personal finance is a huge interest of mine. If you found this interesting or helpful, feel free to send me a message, I love discussing personal finance!